How to Create a c and Stick to It

The Importance of Budgeting for Financial Health

Budgeting is a vital tool for maintaining strong financial health. It gives you a clear picture of your income, expenses, and financial obligations, allowing you to make informed decisions about how you spend and save. By tracking where your money goes each month, budgeting helps you identify unnecessary expenses, cut back on overspending, and prioritize essential needs.

One of the biggest benefits of budgeting is that it ensures bills and other recurring payments are settled on time, helping you avoid late fees and maintain a good credit score. It also encourages consistent saving, which is key to building an emergency fund, planning for large purchases, or investing for the future.

A good budget also helps reduce reliance on debt. When you live within your means and plan your expenses carefully, you’re less likely to rely on credit cards or loans to meet your day-to-day needs. This, in turn, can reduce financial stress and make it easier to manage debt repayment.

In times of uncertainty—such as job loss, medical emergencies, or economic downturns—a well-managed budget offers a financial safety net. It allows you to adjust quickly without falling into crisis.

Ultimately, budgeting is not about restriction; it’s about empowerment. It gives you control over your money, aligns your spending with your values, and helps you work toward your short- and long-term financial goals. Whether you want to pay off debt, buy a home, or simply live more comfortably, budgeting is the first step toward financial freedom .Click https://topviewsolution.com/2025/04/08/essential-tips-for-first-time-home-buyers-in-kenya-guide/

Steps to Develop a Realistic Budget

Creating a practical budget requires a clear understanding of your financial situation . Follow these steps to build a budget that fits your lifestyle and helps you achieve your financial goals .

1. Understand Your Income 💵

The first step in creating a budget is knowing exactly how much money you have coming in each month. This includes all forms of income, such as:

-

Salary or wages from employment

-

Earnings from freelancing or side jobs

-

Rental income

-

Investment income (dividends, interest, etc.)

-

Government benefits (if applicable)

Make sure to consider your after-tax income (take-home pay), as this is the money available for you to budget. If your income varies from month to month (for example, due to freelance work or commissions), calculate an average income based on recent months.

Tip: Be honest about your income sources to avoid budgeting based on overly optimistic figures.

2. Track Your Expenses

The next step is to track where your money is going. Expenses generally fall into two categories:

-

Fixed Expenses: These are predictable, recurring costs that remain the same month-to-month, such as rent or mortgage payments, utility bills, car payments, and insurance premiums.

-

Variable Expenses: These fluctuate based on consumption and lifestyle choices, including groceries, transportation, entertainment, dining out, and personal care.

Tip: Don’t forget small, recurring costs like subscriptions to streaming services, memberships, or daily coffee. These can add up over time.

3. Set Financial Goals

Having clear financial goals will help guide your budget. Whether you’re trying to save for a vacation, buy a home, pay off credit card debt, or build an emergency fund, setting specific goals gives your budget purpose.

SMART goals (Specific, Measurable, Achievable, Relevant, Time-bound) are effective. For example, instead of saying, “I want to save more money,” try saying, “I want to save $5,000 for an emergency fund by the end of the year.”

When setting goals, it’s important to prioritize. If you have multiple goals, focus on the most urgent or important ones first. You may need to adjust your budget to make room for savings toward these goals.

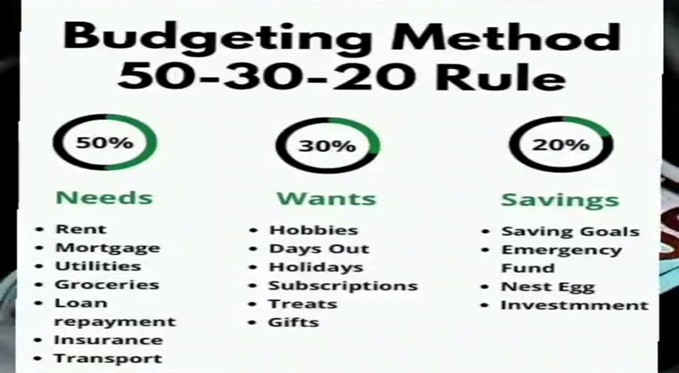

4. Create Your Budget Categories

Now that you know your income, expenses, and goals, it’s time to create your budget. Common categories typically include:

-

Housing: Rent or mortgage, utilities, and property taxes

-

Transportation: Car payments, gas, public transport, car insurance

-

Groceries: Food, household items, and toiletries

-

Insurance: Health, auto, life, and other insurance premiums

-

Entertainment: Dining out, movies, subscriptions

-

Debt Repayment: Loan payments, credit card payments, student loans

-

Savings: Emergency fund, retirement savings, investment accounts

Your budget should reflect both your fixed and variable expenses. Allocate funds for savings and debt repayment in addition to everyday expenses.

Tip: Make sure to treat savings and debt repayment as “fixed” expenses in your budget, just like rent or utilities. This ensures they are prioritized.

5. Balance Your Income and Expenses

Once you’ve listed all your income and expenses, the next step is to balance the two. Ideally, your income should be equal to or greater than your expenses. If your expenses exceed your income, you will need to cut back on discretionary spending or find ways to increase your income (e.g., taking on a side hustle, reducing non-essential costs).

If your income exceeds your expenses, this is a great opportunity to save and invest more toward your goals. Consider directing any surplus toward paying off high-interest debt or adding to your savings or retirement fund.

Tip: If your income is inconsistent, use a lower average monthly income for budgeting. This will ensure that you don’t overspend during months when your income is lower than expected.

Tools and Apps to Assist with Budgeting

Managing your budget manually can be time-consuming, but there are many tools and apps available that can simplify the process. These tools help you track income and expenses, set goals, and stay on top of your finances.

1. Mint

Mint is a widely-used, free budgeting tool that automatically tracks and categorizes your expenses by linking to your bank and credit card accounts. It provides a real-time snapshot of your spending and helps you see where your money is going. Mint also offers insights into your financial habits and helps you set and track your savings goals.

https://www.mint.com

2. YNAB (You Need a Budget)

YNAB is a comprehensive budgeting tool that helps users prioritize their spending and save for goals. The app follows a zero-based budgeting approach, where every dollar is assigned a job. YNAB offers a wealth of educational resources and workshops to help users develop strong budgeting habits. While it’s a paid service, it’s an excellent investment for those serious about mastering their finances.

3. GoodBudget

GoodBudget is a virtual envelope budgeting app that works by allowing you to create different categories for your spending, such as food, entertainment, and savings. Unlike Mint and YNAB, GoodBudget doesn’t connect to your bank accounts. Instead, you manually input your transactions, which makes it a great option for those who prefer a hands-on approach.

4. PocketGuard

PocketGuard automatically tracks your spending by linking to your bank accounts. It helps you see how much disposable income you have after covering bills and savings goals. The app also identifies recurring payments and suggests ways to save money. PocketGuard is a good option for people who want to stay on top of their spending without the complexity of a detailed budget.

5. Google Sheets or Excel

If you prefer a more customized approach, you can create your own budget using Excel or Google Sheets. Many free budget templates are available online that you can personalize. This option allows you to have complete control over your budget and tailor it to your specific needs

Tips to Maintain and Adjust Your Budget Over Time 🔄

Creating a budget is just the beginning ; sticking to it requires regular effort 🏋️♂️. Here are some tips to help you stay on track and make adjustments when necessary ⚙️:

1. Review Your Budget Regularly

It’s essential to regularly review your budget, especially if your income or expenses change. Set aside time once a month to assess your spending, savings progress, and whether your goals are being met. This ensures that you stay on top of your finances and can make any necessary adjustments.

2. Track Your Spending in Real-Time

Use your budgeting tool or app to track your spending as it happens. This will help you avoid going over your budget in any category and allow you to make adjustments in real-time. The more actively you track your spending, the more likely you are to stick to your budget.

3. Cut Back on Discretionary Spending

If you find that you’re overspending in some areas, it’s time to review your discretionary expenses (e.g., dining out, entertainment, shopping). Find ways to reduce costs without sacrificing your lifestyle entirely. Small sacrifices, like cooking at home or reducing subscription services, can free up more money for savings or debt repayment.

4. Adjust for Life Changes

Life is unpredictable, and sometimes your financial situation changes. Whether it’s a job loss, an unexpected expense, or a windfall (e.g., tax refund), it’s important to adjust your budget to reflect these changes. For example, if you get a pay raise, you might choose to allocate more toward savings or paying off debt.

5. Avoid Lifestyle Inflation

When your income increases, it’s tempting to upgrade your lifestyle—buying a new car, renting a more expensive apartment, or taking more vacations. This is known as lifestyle inflation. While it’s okay to enjoy some improvements, be mindful of your long-term financial goals. Resist the urge to overspend as your income rises.

Conclusion: Long-Term Benefits of Disciplined Budgeting

Budgeting is not just a way to manage your finances—it’s a strategy for achieving your financial goals, whether that means saving for a down payment on a house, building an emergency fund, or retiring comfortably. By creating a realistic budget and committing to it, you gain control over your money and reduce the stress associated with financial uncertainty.

The long-term benefits of disciplined budgeting include:

-

Financial security: A budget helps you save for the future and build a safety net for emergencies.

-

Debt reduction: Budgeting allows you to prioritize debt repayment, helping you eliminate high-interest debt more quickly.

-

Better financial decisions: With a budget in place, you can make informed choices about your money and avoid impulse spending.

Ultimately, a well-maintained budget is a roadmap to financial freedom . By reviewing and adjusting it regularly , you can ensure that you stay on track toward achieving your goals and living a financially secure life 🏖️.Read morehttps://topviewsolution.com/2025/04/08/role-of-microfinance-institutions-in-kenyas-economy/

Disclaimer:

The information provided in this article is for general informational purposes only and does not constitute financial advice. While every effort has been made to ensure the accuracy of the content, readers are encouraged to consult with a qualified financial advisor before making any financial decisions. The author and publisher are not liable for any financial losses or decisions made based on the information provided herein.